From shopping, to ordering food, to notarizations – the global COVID-19 pandemic made electronic transactions a regular and expected part of our lives. For Notaries and their customers, remote notarizations became an option to complete notarizations during the height of the pandemic, when face-to-face interactions sometimes became difficult due to local lockdown measures.

While many states now allow remote online notarizations (RONs) through permanent laws, you may not realize that you were already empowered to perform another form of electronic notarization. In-person electronic notarization (IPEN) has been around for more than 20 years and is approved for use in all 50 states in some form (check your individual state’s laws for the specific requirements for IPENs or other electronic notarizations).

The idea of IPEN was born during the 1990s digital revolution. With the creation of the internet and other digital tools, IPENs were seen as a way to create greater trust in notarial acts. And they were on their way to being widely accepted, but the twin disasters of the bursting real estate bubble and the robo-signing scandal in the mid-2000's, set back the wide adoption of IPENs. However, with IPEN laws on the books, this type of notarization is just waiting for another chance at adoption.

IPEN and RON explained

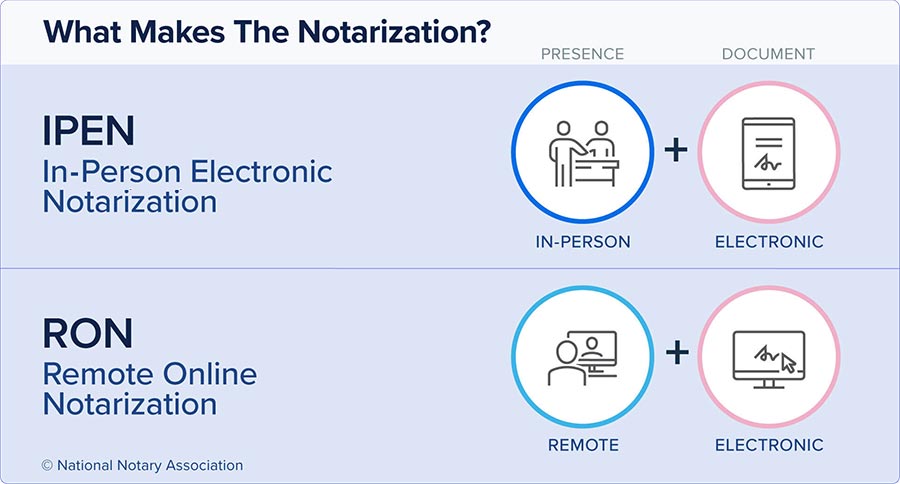

IPEN and RON aren’t the same thing. While they share some similarities — namely being electronic notarizations — they have fundamental differences.

IPEN (in-person electronic notarizations) means exactly what it says. They are in-person notarial acts. In other words, they require the signer to appear in front of the Notary in the same physical location at the time of the notarization, and be identified by the Notary in the same way as a traditional notarization. The documents are presented in a digital format and signed using an electronic signature. The Notary uses an electronic seal and signature to notarize the document.

RONs (remote online notarizations) are notarial acts that allow the signer to “appear” before the Notary over the internet using audio-visual technology. A RON does not require the signer to be in the same physical location as the Notary. Depending on state law and the service being used, the process involves the system establishing the identity of the signer prior to interacting with the Notary, who also verifies the signer’s identity using the same identification documents that are required for a traditional in-person notarization. The signer “signs” the document electronically and the Notary affixes his or her electronic signature and seal to the digital document. The audio and video of the notarial act is typically recorded.

RON has received more attention of late due mainly to the worldwide COVID-19 pandemic when many states had temporary emergency authorization for remote notarizations.

Many of the states that put temporary remote measures into place have since enacted permanent laws. To date, 46 states have RON laws on the books.

However, mortgage industry players and the big banks have been slow to utilize RONs in a widespread way, due to the inherent technical complexity of a RON, the lack of a 50-state operational footprint, concerns in some quarters that remotely notarized documents may not be legally recognized across all state lines and other factors.

Making a comeback

In the words of LL Cool J, “Don’t call it a comeback, I’ve been here for years”. But why is IPEN growing in popularity now? There are a number of reasons.

First, title companies are looking for ways to be more efficient, and IPEN offers both efficiency and a legally verifiable signing process while maintaining their relationships with key partners.

Second, IPENs allow loans to close and be sold to investors in the secondary mortgage market just as quickly as RONs, and there aren’t the same concerns with documents notarized with IPEN being rejected when they cross state borders as some have raised with RON.

Third, and just as important, IPEN makes the process easier for Notaries with a robust, intuitive, reliable platform that improves efficiency.

Further, there’s a need for IPEN. Prior to the pandemic about 70% of loan closings were done at the lender’s or title company’s offices. Now that number is about 50%, with the remaining occuring in-person, but outside the traditional office. A robust, intuitive, flexible, and secure digital solution that utilizes traditional Notary practices makes IPEN an attractive option for title companies, recorders, signers, and Notaries alike.

How IPEN works

An illustration of how an IPEN works from beginning to end will clearly show the benefits of the process. Because this article has discussed IPEN’s growing acceptance in the mortgage industry, I will use a loan signing as an example:

Step 1: The title company or closing agent loads the loan documents in digital format into a technology platform (either its own or one provided by a third-party vendor such as EscrowTab) that will be used for the signing and assigns it to the Notary Signing Agent.

Step 2: The Notary Signing Agent reviews the documents that are ready for the signer on the platform. If there is a last-minute change to a document prior to the loan signing appointment, there is no need for the Notary to print a revised form, or pick up the revised document at a FedEx location. The documents are updated by the title company or closing agent instantaneously and uploaded to the platform prior to the signing.

Step 3: The Notary Signing Agent travels to the borrower for the signing appointment, logs in to the platform from which the electronic documents will be presented to the borrower and signed, and verifies the identity of the borrower in exactly the same way as they would for a traditional notarization.

Step 4: The Notary Signing Agent walks the borrower through the documents in the loan package appearing on the Notary’s device. The borrower signs the documents electronically and the Notary Signing Agent performs any notarizations that are required electronically. The devices that can be used might vary from one platform to another

In addition, digital closing systems can perform quality control checks, verifying that all the signatures and fields have been filled in, eliminating potential errors and giving the Notary and the signer the confidence that the notarization has been completed properly.

Step 5: Once the documents are signed and notarized on the platform, the title company, closing agent, and lender are notified that the documents are signed and ready for their review.

While I have used a loan signing as an example, IPEN can be used for the notarization of a document in any industry setting.

Verifiable signatures

In the early 2000s, there was pushback by some states because the statutes hadn’t caught up to the technology. But that isn’t the case anymore.

One of the specific benefits that was first realized with IPEN technology, and then adopted by RON technology later, is that the electronic signatures and notarizations can be verified. An entire audit trail of all actions taken on the electronic document by all the parties is created at the time they occur and can be reviewed by others. This imparts trust to electronically signed and notarized documents that is simply not possible with paper documents.

Before You Get Started

Before you perform IPENs, make sure that you’ve reviewed the laws of your state to determine whether you can perform in-person electronic notarizations. There may be a process you must follow to qualify with your state’s Notary commissioning official, a training course you may be required to take, and an exam you may have to pass. You’ll also want to read up on what your laws say about completing journal entries and notarial certificates for IPENs, as well as any other rules you must follow. Most of the technology providers can also help you through this process.

Once you learn your state’s statutes and regulations related to IPENs, you can begin the process of getting on board with the technology you will need to perform IPENs. This typically will be through any companies you work with that are using IPEN.

Depending on the technology provider, you may need specific hardware to perform IPENs. It could be a laptop or mobile computing device. The information can be obtained from the technology provider, such as EscrowTab.

You also will need an electronic seal. Depending on the state, you could receive your electronic seal from the technology provider or obtain it from the NNA.

Then you can sign up with the provider of your choice. (EscrowTab does not charge a fee to create an account, and once created, other signing platforms can see that you are able to perform electronic notarizations.)

Notably, although the focus of this article has been the use of IPEN in the mortgage market, that doesn’t mean IPEN can’t be used in other industries. Because IPENs replicate traditional notarizations, more markets can use and accept IPENs.

But more than that, you’re future-proofing your business by being ready for what your clients expect and positioning yourself at the front of the pack compared to other notary signing agents.

How IPEN benefits Notaries

IPEN saves time and money for Notaries, especially Signing Agents. For example, there is no need to print documents or pick up loan packages from the title company. If a document needs to be updated, it can be done electronically.

So, what does this mean for the Notary? Fewer business expenses, documents that are ready and correct, more on-time appointments, and happier signers. With the time you save by not having to print documents or pick up new loan packages, you can schedule more jobs, improving your profitability.

Notarizations Enter the Digital Age

Remote online notarization demonstrated that there was an appetite for electronic notarizations, but in-person electronic notarization shows how they can be done in a way that is easy and secure — and most of all familiar, because IPENs allow Notaries to follow the same practices and procedures in performing notarizations that they have done for years.

The Notaries I’ve worked with love IPEN for all these reasons, and I expect that the demand will transform Notary businesses, making them more efficient and profitable without sacrificing the trust and security that is expected from the work of professional Notaries.

Brendon Weiss is a Co-Founder of EscrowTab. EscrowTab provides title companies and lenders a software solution to close loans electronically nationwide using its in-person electronic notarization (IPEN) solution.

Additional Resources:

Traditional notarization, IPEN and Remote Online Notarization: How they work